Fueling your company’s urge to surge

Occasionally, a business overtakes its competitors and moves from industry player to industry leader. Southeast Asia points the way for how to achieve this.

Photo illustration by twomeows

Imagine you are a business leader operating a decade from now. Your organization has become the unassailable leader in its market. How did this happen?

In years past, you were competing head-on with several other players. Each time you tried to move ahead, your competitors kept up with you. You watched what they did, and if you noticed them doing something new, you would try it out yourself to make sure they didn’t build a lead over you.

But now, you have left your competitors behind. Your organization has been able to command higher margins and win business more easily. Suppliers and financiers beat a path to your door. The best talent wants to work for you, and you can afford to pay them more than your competitors can. If this continues, you may be able to dominate your industry for decades to come.

This story is an example of a pattern that we have observed. Whether it’s football teams, car manufacturers, oil majors, fast-moving consumer goods companies, or retailers, we see the same emergence of (typically) three to five players in major markets, displaying similar levels of growth, profitability, and market share. But just occasionally, an organization surges ahead of its competitors, moving from industry player to industry leader, securing a position in which it demonstrates a clear and sustainable lead.

Many of the companies that we have observed carrying out such surges have been able to take advantage of turbulence in the environment to move ahead of competitors. The COVID-19 crisis is the most turbulent period for business since World War II — and it’s already clear that some sectors are experiencing surges of a sort as a result. (Think of the recent spike in revenue at supermarkets, or of the sudden popularity of video conference services.)

We are not suggesting that a surge should be part of an organization’s response to the COVID-19 crisis. Companies should be taking a series of positive steps, such as evaluating the supply chain and assessing workplace locations — two of seven measures described in March by PwC’s Global Crisis Centre.

Indeed, most businesses are focused on survival at the moment. The key question is how to learn from those companies that have surged in the past in order to help bring about a focus on the essential, or pivot to a new set of products and services supported by your existing capabilities, or come together with other companies in your industry or supply chain.

Doing this will require boldness and the ability to convince others to come with you. This article may help you to think through your surge options, and provide inspiration from those who have gone before.

When we talk about companies that have surged, we don’t mean startups that have been growing fast since inception. Rather, we mean middle-aged companies. They have already climbed a growth curve as they matured. But now they have managed to create and climb an entirely new growth curve.

Many companies around the world have done this. The seminal 2001 book Good to Great: Why Some Companies Make the Leap...and Others Don’t, by Jim Collins, studies several U.S. examples in detail, focusing on those that had made the leap to great results, and sustained that performance for at least 15 years.

What is the secret ingredient that enables this “surge” to happen? How does it happen, when does it happen, and — keeping in mind that we don’t yet know what the full fallout from the coronavirus global health emergency will be — how can organizations position themselves for a surge?

In an attempt to answer these questions, we have focused on Southeast Asia, a region with a rich and varied collection of companies founded decades ago, some of which have experienced significant surges. Many are family owned or family controlled. Others have significant government or sovereign wealth fund shareholders and operate in a more complex environment than that described in Collins’s book, which didn’t cover any non-U.S. or privately owned companies and which focused on corporate performance in the pre-Internet era, from the 1950s to the 1990s.

Southeast Asian surge

The qualities above make these Southeast Asian companies especially worth studying. They help us understand how a business becomes a candidate for a surge — and whether your company might be one too.

Many companies in the region — home to the 10 countries that make up the Association of Southeast Asian Nations (ASEAN) — are now finding their own backyard is too small. They are therefore not merely exporting to the rest of the world, but also setting up or taking over businesses around the globe.

Thailand’s Charoen Pokphand Group has become a large foreign investor in China and owns businesses in the United States and United Kingdom. It continues to seek new investment opportunities, as highlighted by its recent purchase for US$10.6 billion — in cash — of U.K. supermarket operator Tesco’s hypermarket business in Southeast Asia.

Ayala, one of the largest conglomerates in the Philippines, has for some time been investigating opportunities in Europe’s high-tech automotive sectors, including design capabilities in electric vehicles. Jollibee Foods, a Philippine fast food group, in 2019 said it would buy the Coffee Bean & Tea Leaf, a U.S. chain of specialty shops, in what would be its largest overseas acquisition so far.

Both AirAsia of Malaysia and Lion Air of Indonesia have spread their wings beyond their home countries, developing innovative ways to operate in multiple markets despite regulatory barriers. And in Vietnam, the country’s largest conglomerate, Vingroup, pursues a surge strategy of being the number one or two in its chosen markets. It is perhaps not a surprise to learn that Vingroup’s founder (and Vietnam’s richest man), Pham Nhat Vuong, recommends that his employees read Collins’s book.

Seven factors that enable a surge

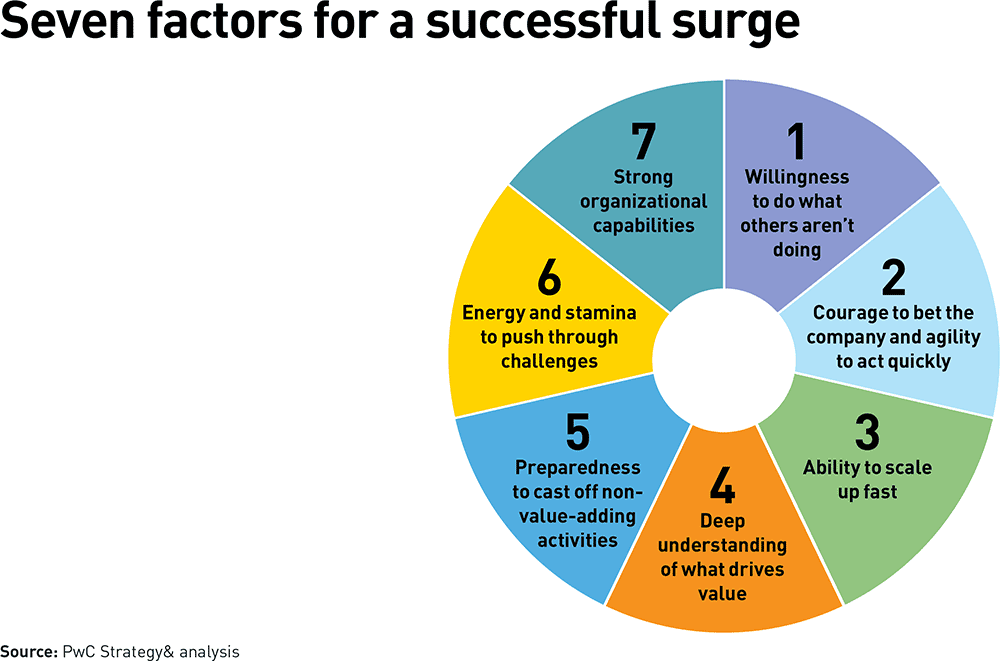

Our research, reading, and interviews with chief executives who have led surges have uncovered seven factors that can enable a successful one (see “Seven factors for a successful surge”).

Factor 1: Willingness to do what others aren’t doing

Most companies we look at that don’t surge are obsessed with their competitors. They compare pricing, products, marketing initiatives, and, if they can, costs and operating models. They seek to stay one step ahead (or at least not more than a step or two behind) their competitors. They are completely focused on market share.

But companies that surge don’t think like that. They don’t look at their competitors, at least not quite so obsessively. They look at their customers, or potential future customers, and focus on how they can provide better value for the customer — profitably.

Companies that surge look at their customers, or potential future customers, and focus on how they can provide better value profitably.

AirAsia is a good example of this. The low-cost airline was cofounded in 2001 by Malaysia-born entrepreneur Tony Fernandes and has capitalized on the growth of a middle class in ASEAN — people who could, for the first time, afford air travel.

AirAsia spotted what legacy airlines had not spotted or had chosen to ignore. Rather than simply offering travelers dozens of cheap flight connections between capitals and major commercial centers in the region, AirAsia decided to provide not only such connections but also flights to and from second- and third-tier cities where there hitherto hadn’t been a discernible demand. That was because their populations were too small and per capita income too low to support air travel.

Such locations appealed to AirAsia for two reasons. First, the region’s emerging middle class was not only a big-city phenomenon. Per capita income was also growing in second- and third-tier cities. Second, it was starting to become clear that demand for travel was likely to grow between those locations as people sought medical treatment or new employment opportunities, or wanted to visit extended family and relatives. Visa-free travel within ASEAN for the bloc’s citizens was also a helpful factor.

With the launch of AirAsia’s services, a patient wanting medical treatment in Malaysia could fly from Padang, on the western coast of the Indonesian island of Sumatra, to Kuala Lumpur in less time than it would take to fly to Jakarta, the Indonesian capital. People could also fly from the central Vietnamese city of Danang to Malaysia to access that job market, without having first to travel to the Vietnamese capital, Hanoi, or commercial capital, Ho Chi Minh City, for a flight to the Malaysian capital. Naturally, AirAsia had to be able to offer such routes at prices that would appeal — and it did just that, as a no-frills carrier in the mold of Europe’s easyJet and the U.S.’s Southwest Airlines. AirAsia’s marketing slogan, “Now everyone can fly,” reflects the reality that the company has made distance travel possible for millions of people for whom flying was previously unaffordable.

Of course, focusing on customers rather than competitors is not a new strategy. But many companies still pay far too much attention to their competitors. In many cases, the board carries some of the blame. It’s tempting for board members to look for yardsticks in order to measure whether management is doing a good job — and the easiest yardstick is the competition. Enlightened boards don’t focus their managers on the competition. Instead, they ask what innovations and changes the company can introduce to increase the value it offers to its customers.

Factor 2: Courage to bet the company and agility to act quickly

Many established companies are risk averse. They adopt risk management processes, report quarterly to shareholders, and are careful not to disturb their market positioning in the eyes of investors. Having the courage to bet the company on a new product or service that fundamentally transforms a business and enables it to grow multiple times larger is rare. Even if the courage can be found, the bet is hard to pull off given the questions that boards and lenders will ask. However, we have found that companies in ASEAN markets can often make bet-the-company decisions quickly because family control means that a close-knit group drives the key decisions.

One example of this is IOI, a listed, family-controlled Malaysian conglomerate active in palm oil and oleochemicals. After starting slowly in 1997 with an initial oleochemical plant acquisition in Malaysia, IOI became one of the largest oleochemicals groups in the ASEAN region between 2001 and 2007, increasing its revenue nearly sevenfold by making a series of opportunistic purchases of oleochemicals businesses in Europe. The first move came in 2001, when a Malaysian palm oil, logistics, and automotive conglomerate launched a hostile bid for Palmco, a refinery in which IOI held a 30 percent stake. IOI launched a counteroffer only a few days later, taking on significant debt in order to enter a bidding war that it eventually won, gaining a controlling stake in Palmco and doubling IOI’s revenues in the process. The following year, IOI acquired oils and fats business Loders Croklaan from Unilever for a price equivalent to one-third of IOI’s annual turnover. These two acquisitions were then built upon with further acquisitions to create one of the largest global suppliers of specialty fats.

Factor 3: Ability to scale up fast

Significantly growing a business is one thing. Doing so quickly is another.

Vingroup of Vietnam decided in 2014 to move into the grocery market from its core retail and property business. Within three years it had opened over 800 minimarts, cementing its market dominance in the subsector.

The challenge with scaling at speed is that it can uncomfortably stretch management, financing lines, and the existing business. Acquisitions need to be integrated and developed through deliberate capacity building. Trusting, deep relationships should have been built among core management team members before the surge effort — then, when it’s time to quickly scale up, a friction-free set of actions can be taken by the team; everyone knows their role and what they should be doing.

Yeow Chor Lee, chief executive of IOI, said that a key part of his success was learning how to acquire and incorporate new businesses into the group by keeping things simple, so that once an acquisition was made, the extraction of synergies was rapid. For example, he eschewed developing complex post-acquisition integration plans in favor of assembling lean teams of senior managers who together worked through issues as they arose.

Factor 4: Deep understanding of what drives value

We found a great discussion of the differences between truth and commonly accepted but wrong industry norms in Jules Goddard and Tony Eccles’s book Uncommon Sense, Common Nonsense. The authors point out that all industries have a set of beliefs that are accepted as self-evident by the players in that industry. Some of these beliefs are true (common sense) and some are false (common nonsense).

In many cases, the false beliefs were once true beliefs. But those truths became obsolete as technology, regulation, or markets moved on. Some companies identify this pattern and develop a new and accurate view that is still not recognized by their competitors in the industry (the authors refer to this as uncommon sense). Companies that surge often do so because they have developed an uncommon sense of what customers value.

Sheng Siong, a Singapore supermarket chain, is a good example of a company with this uncommon sense of what its customers want. Founded in 1985, the family-owned business grew from its roots in pig farming to become the third-largest supermarket chain in Singapore by 2008 — the year the global financial crisis hit. One of its early innovations was to combine in one location a “wet” and a “dry” market, where fresh produce and household goods were sold under one roof — a clever convenience in a city-state where shoppers hitherto had to visit two different locations to meet their shopping needs.

In the three years following the crisis — a period in which Singapore’s retail market saw little growth — Sheng Siong managed to increase turnover by about 50 percent, while gross profit margins expanded. It did this in part by speeding up service at its outlets as a way of increasing turnover per square foot of supermarket space, which in turn allowed Sheng Siong to keep prices low. It also introduced 24-hour shopping, and ensured that customers rarely had to wait in line — a phenomenon that Lim Hock Chee, founder and chief executive, is reported to have attributed in part to Sheng Siong having “the fastest cashiers in Singapore.”

Lim is a strong believer in building his own capabilities — a quality discussed in Factor 1 above. His view, expressed in a 2014 interview with the local Straits Times newspaper, was: “Rather than waste time comparing ourselves with others, why not look at how you can improve yourself?”

Factor 5: Preparedness to cast off non-value-adding activities

In many cases, a surge is prevented because a company is unable or unwilling to shed a line of business or suite of activities that is no longer profitable. These non-value-adding legacy activities can weigh down management to the point where it has little time to pursue value-adding businesses.

An example of powerful growth unleashed by disposing of a line of business was Telekom Malaysia’s (TM’s) divestment of Telekom Malaysia International (now Axiata) in 2008. This allowed TM to focus on its domestic business and the government-supported rollout of fiber-optic services across the country. The company’s shares rose significantly as a result. This divestment forced management to focus on maximizing the domestic business without being distracted by the mobile phone business. In the meantime, Axiata moved ahead to become a large mobile phone operator in multiple Asian countries.

Factor 6: Energy and stamina to push through challenges

Collins’s examples of surging companies in Good to Great emphasized that making the leap can take a long time, and that, though it includes a rapid scaling-up (Factor 3), the actual surge process can be a multiyear marathon rather than a sprint. At the end of the marathon, it’s clear that victory has been achieved. But during the process, it’s not necessarily obvious that the company is doing something extraordinary.

Across ASEAN, we have also seen, time and again, that major surges are driven by family-controlled companies in which a vision of what needs to be done is sustained for years by a closely related group of people.

Sudhitham Chirathivat, retired chief executive of the Central Group, a Thai operator of food and fashion stores, said in a 2014 interview in the Bangkok Post, “Our father Tieng taught us to love and respect each other in the family.... On top of that, in business, he taught us that we first needed to support our own siblings before our own offspring.”

This closeness — reinforced by many of the extended family members living together and the existence of a family council to oversee the group — meant that Central Group was able to deliver multiple surges during the period between 2011 and 2017, despite Thailand going through major political disruption in 2014 and despite the death of the company chair in 2012. During this period, Central Group entered Europe with the purchase of Italy’s Rinascente department stores and, in 2015, of Germany’s Karstadt Premium group of stores, which included the flagship KaDeWe store in Berlin. In 2015, the group also entered Vietnam with the acquisition of the Nguyen Kim and LanChi Mart stores. Over the same period, the group’s share price increased sixfold.

Factor 7: Strong organizational capabilities

Multiple interviewees told us the same thing about their organization — that they were able to grow because they had strong capabilities and knew what they were. Those capabilities related to the management team’s ability to quickly absorb and turn around new acquisitions, or ability to act fast when unexpected opportunities arose, or ability to work closely with governments and support their agendas in what is often referred to in the region as “nation-building.”

However, we also heard that it is important to work within those capabilities. Richard Curtis, chief executive of CMS, a Sarawak, Malaysia–based cement manufacturer that diversified into property and infrastructure in the 1990s, shared examples of areas that the company decided against entering when opportunities cropped up as it was looking at further growth from 2007 to 2014. These areas included manufacturing smartphones and expanding into Cambodia — and the company’s competencies did not support those expansions. Likewise, IOI was presented with many opportunities to expand into Indonesia but decided to focus on Malaysia, where it had a deep understanding of how to do business.

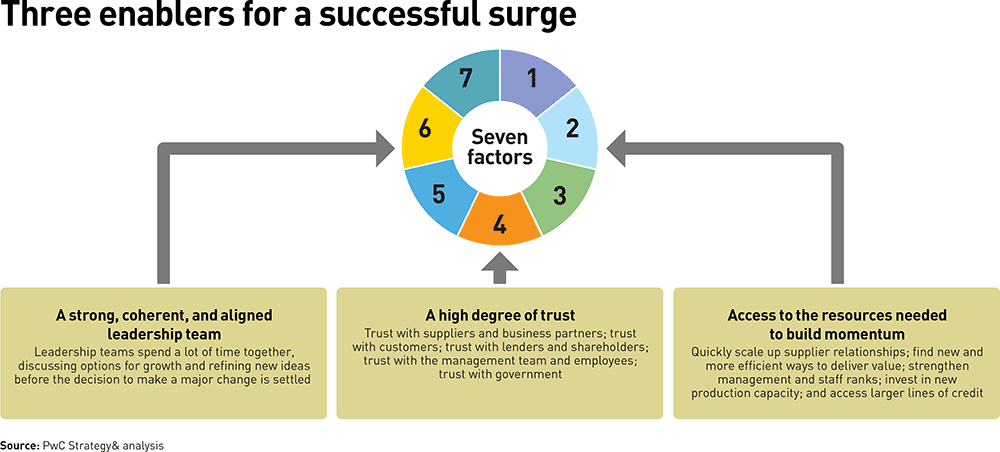

The seven factors above are all important in a surge. Our research has also shown that they work best when supported and driven by three enablers (see “Three enablers for a successful surge”).

Enabler 1: A strong, coherent, and aligned leadership team

An organization can surge only when leadership decides to make a big bet, and this cannot be done properly unless the whole leadership team is aligned.

We have seen several models for alignment — both top-down (a senior person directs and everyone else follows) and horizontal (consensus-based). But in most of the companies we have observed, leadership teams spend a lot of time together discussing options for growth, learning from each other, and refining new ideas before making the decisions that result in a surge.

The year 2014 was illustrative of this. It was when three Singapore-listed, Asia-based agribusinesses — Olam International, Wilmar, and Noble Group — separately started to challenge the long-standing global dominance of Western agribusinesses (Cargill, Archer Daniels Midland [ADM], Louis Dreyfus, and Bunge) through a series of big acquisitions. These deals were a key element in the surges of these Asian companies.

Olam, led by chief executive Sunny Verghese, snapped up for $1.3 billion the cocoa-processing business of ADM, turning it into one of the largest producers of key chocolate ingredients. Wilmar, controlled by Malaysia’s Kuok family, acquired Australian food group Goodman Fielder for AUD$1.4 billion (about US$1.3 billion). Both were bold moves that required strong vision and leadership.

In addition, it is unusual for a team to build itself to the point where it can surge in a short time. Usually we see the core of a team building itself over several years — as in the case of Olam. However, the catalyst for a big bet can be a change in the dynamics of leadership, for example, when a new generation takes over leadership of a family company, even when the previous generation remains in an oversight or advisory role.

Enabler 2: A high degree of trust

Our interviews with many of the companies in this article covered the element of trust. Trust is needed with all the key stakeholders with which the business deals. A surge involves trust with suppliers and business partners so that they are willing to quickly increase engagement. It involves trust with customers, particularly if the surge means new and different models for doing business. It also involves trust with lenders and shareholders, trust between the management team and employees, and, in some cases, trust with government.

Trust is earned over time, and requires relationships to be cultivated and tested. Members of this trust ecosystem will particularly value the relationships when they have been through difficult times together. For example, First Philippine Holdings, an energy, land, and construction conglomerate, saw its major businesses confiscated by the Philippine government in 1973. That resulted in the company coming close to collapse over the following decade. The memory of this hardship, and the subsequent success in rebuilding, brought key management figures together.

Externally, trust is also critical. “Shine brightly when everyone else is in the dark,” said Michael Yam, for many years chief executive of Sunrise Property, part of Sunrise Berhad in Malaysia, in one interview. During the 1997 Asian financial crisis, Sunrise continued, despite great financing challenges, to build and pay its suppliers even as others were walking away from projects, leaving partly built concrete shells that littered the Kuala Lumpur cityscape for years afterward. As a result, Yam built an unprecedented level of trust in his company among banks, customers, and suppliers, which enabled Sunrise to prosper for many years.

Enabler 3: Access to the resources needed to build momentum

One of the biggest problems experienced by fast-growing companies is that they can’t keep up with their own growth. They find the magic formula to massively increase customer demand, but simply can’t keep up with the demand, and so the intended surge fizzles out.

To really build momentum, a company needs to quickly scale up its relationships with suppliers and find new and more efficient ways to deliver value to its customers, rather than simply working harder using its former business processes and approaches. This means that suppliers need to be prepared to stick their necks out, increasing their capacity (which may in turn require them to invest or recruit) so that they can keep up with the surge that their customer is generating. The company driving the surge will also need to quickly strengthen its management and staff ranks, invest in new production capacity, and handle much larger lines of credit with its downstream supply chain.

One example is Dyson, manufacturer of household appliances. Though not a homegrown Southeast Asian company — it was founded in Britain and is considered a British company — it does rely on Malaysia and Singapore for most of its manufacturing and is moving its headquarters to Singapore in 2021, and thus can be seen as Southeast Asian in terms of operational footprint. Dyson quadrupled its global revenues in the three years through 2018, driven in part by identifying and exploiting a market for premium hairdryers and hair stylers. That meant suppliers having to quickly gear up to meet this demand. From the time it started manufacturing in Malaysia in 2003, Dyson built close relationships with local partners such as its contract manufacturers. The company designed production lines with them, and controlled procurement and production processes too. Dyson also ensures that its suppliers can grow by training them to manufacture its products. As a result of this close partnership, when Dyson faced rapid growth, its suppliers were prepared and able to scale up their production accordingly.

Being ready to surge

Being the unassailable leader is certainly an attractive goal, but is your organization ready to surge? Four simple questions will help you identify whether this is the right time to push forward.

First, do you want to surge? You and your management team will need to be prepared to step out of your comfort zone and persuade others to get behind you. You’ll need a clear vision of where the surge will take you — and what your “right to win” is that will get you there. Are you simply going to be the best in your current industry? Or are you going to redefine the industry around your capabilities and unique insights — your uncommon sense — so that nobody can catch up with you?

Second, is the timing right? Picking the right time to move away from your competitors is important. Signs of the right timing include competitors going through internal or external struggles that mean they won’t be able to respond when you make your move. Another sign is anticipated regulatory changes that enable you to take advantage of a new situation quickly. The right timing may also be a generally unfavorable time. Many businesses have moved ahead during recessions and credit squeezes, when they are able to acquire assets and businesses cheaply and use the challenge of difficult times to make difficult decisions, such as shedding unproductive activities. That’s what Michael Yam of Sunrise means by “shine brightly when everyone else is in the dark.”

Third, do you have the right team in place? This means both your internal team and your wider team of customers, suppliers, and service providers. Have you built up the high levels of trust that mean that they are ready to stick their necks out when you stick yours out? Are they willing to give you the benefit of the doubt? Do they recognize that you have uncommon sense from which they can profit by working with you?

Finally, what is the catalyst that’s making you want to surge? Is it the development of a new technology or business model? An expected regulatory change on which you believe you are well positioned to take advantage? An event that has weakened key competitors? Or a recent change in management, involving those who have grown up in the organization (whether members of a controlling family or long-serving team members) who see new opportunities and are prepared to take the steps to exploit them that the previous generation of management wasn’t prepared for?

What comes next

Preparing for a surge is a process that takes time. To start with, we recommend drawing inspiration from those that have done it before. Our recommended reading list below is an excellent first step.

Think about the concrete actions that your organization will take — whether it be a roll-up strategy of taking over similar firms in the markets you wish to dominate, an organic growth strategy, or a venture capital–style “buy the market” approach. This will help you to map out the likely path to a surge.

After that, push forward to execute and, in 10 years, be prepared to look back and be amazed by how far you have come.

The literature of surge

A select group of authors have addressed the key question of how a large, successful organization moves itself to a new level of performance. Jim Collins and his team have spent many years studying this topic and have produced several books following the initial Good to Great text. We found very helpful thinking from several London Business School academics, such as Costas Markides’s Game-Changing Strategies and (as mentioned earlier) Jules Goddard and Tony Eccles’s Uncommon Sense, Common Nonsense.

Here is a recommended reading list that may help you think through your business and the key questions you need to ask before you embark on a surge.

Jim Collins, Good to Great: Why Some Companies Make the Leap...And Others Don't (HarperBusiness, 2001).

Jules Goddard and Tony Eccles, Uncommon Sense, Common Nonsense: Why Some Organisations Consistently Outperform Others (Profile Books, 2013).

Paul Leinwand and Cesare Mainardi, Strategy That Works: How Winning Companies Close the Strategy-to-Execution Gap (Harvard Business Review Press, 2016).

Paul Leinwand and Cesare Mainardi, The Essential Advantage: How to Win with a Capabilities-Driven Strategy (Harvard Business Review Press, 2010).

Constantinos C. Markides, Game-Changing Strategies: How to Create New Market Space in Established Industries by Breaking the Rules (Jossey-Bass, 2008).

Hugh Peyman, China’s Change: The Greatest Show on Earth (World Scientific, 2018).

John Zinkin, Better Governance Across the Board: Creating Value Through Reputation, People, and Processes (De Gruyter, 2019).

John Zinkin, Challenges in Implementing Corporate Governance: Whose Business is it Anyway? (Wiley, 2012).

Author profiles:

- Edward Clayton is a partner with PwC Malaysia. He supports the growth of clients in Southeast Asia, focusing on transport, infrastructure, and consumer-facing industries.

- Jeremy Grant is international editor of strategy+business, based in London.