Growth strategies for an uncertain world

Internationalization can help businesses rethink their global footprint and governments attract trade and enterprise.

Illustration by Flavio Coelho

It was expected, perhaps, but still startling. In its 22nd Annual Global CEO Survey (pdf), PwC asked 1,378 top business leaders from around the world which territories (excluding their own) they considered the most important for their company’s growth prospects in the next 12 months. The world’s chief executives were noticeably noncommittal. As many as 15 percent of them answered “don’t know” in 2019, up from 8 percent the previous year.

CEOs in the United States were even more dubious: 14 percent of them didn’t consider any other markets suitable for growth, up from only 2 percent in the 2018 survey. And around the world, the three growth prospects that had regularly topped the list in previous years — the U.S., China, and Germany — were suddenly much less popular. Other locations, such as Brazil, India, and Canada, moved up in the rankings.

This shift in attitude is already reflected in business investment. Of the 31 percent of CEOs who said they were “extremely concerned” about trade wars, 45 percent said they were shifting their supply chain strategy, and 25 percent said they were shifting their growth strategies to other territories.

One might assume these changes are reactions to the disruptive sweep of geopolitical turbulence. Trade wars and protectionism are forcing a rapid realignment of supply chains and global business footprints. Aspects of globalization that were taken for granted as recently as last year — continued growth in China, manufacturing integration between East and West, the primacy of consumer demand in advanced economies — are rapidly giving way to a new uncertainty. Given the attention being placed on tariffs, particularly between the U.S. and China, companies are reassessing their risk profiles, their trade and investment routes, and their expectations for where growth might still be found.

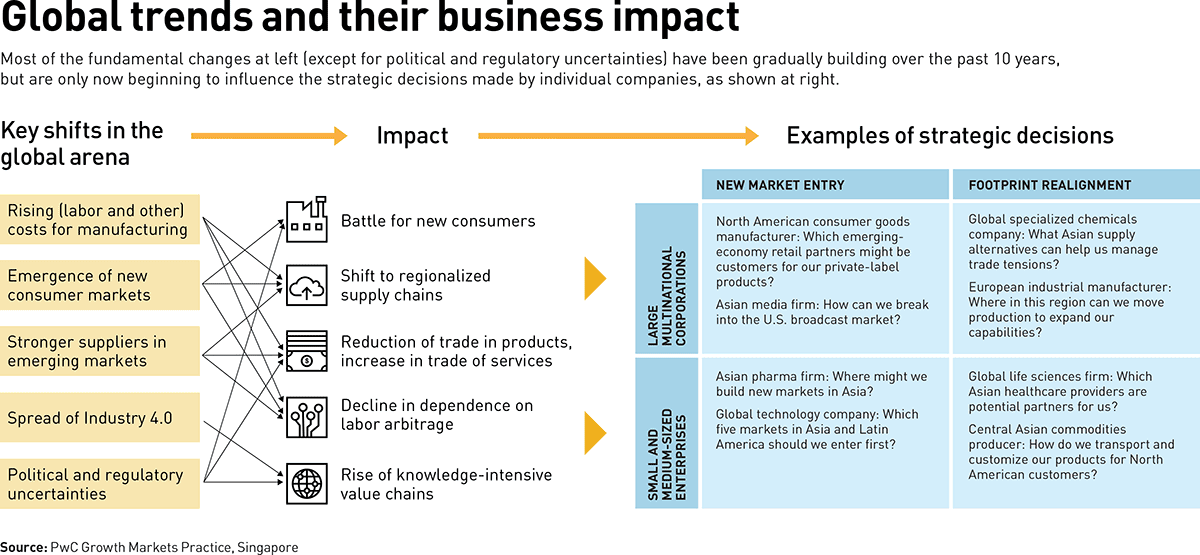

But these new business strategies — and the corresponding initiatives by governments in emerging markets — are not just reactions to recent events. Fundamental aspects of the global economy have been shifting for more than a decade. Elements undergoing change include costs for manufacturing (including labor costs, which are rising), new technological platforms (such as those associated with Industry 4.0), stronger suppliers and other businesses in emerging markets (which are maturing), middle-class consumer populations around the world (which are growing rapidly in emerging markets and shrinking in other places), and political and regulatory uncertainties. Because these shifts took place during and just after the global financial crisis of 2008, they did not get much attention. Although some companies acknowledged them and adjusted their strategies accordingly, many others chose instead to focus on operational improvements and near-term profitability.

A new model of market expansion strategy — we call it “internationalization” — is replacing the globalism of the early 2000s. This model acknowledges that the global business ecosystem now includes many small and medium-sized enterprises and ambitious family businesses, often based in emerging markets, linked together by collaborative supply chains and platforms. At the same time, larger companies with established global supply chains have realized that they need to bring their operations closer to the demand they are targeting. The trade tensions of 2019 have heightened awareness of these dynamics, and accelerated the business response to them (see “Global trends and their business impact”).

Internationalization is an appropriate strategy in this context. It means paying more attention to regional opportunities, and moving activity to places businesses might not have favored in the past. To be sure, global trade will still thrive, but there will be much more regional concentration. Rather than shipping goods around the world from cheap-labor hubs, companies manufacture goods for Asian customers in Asia, for European customers in Central Europe, and for North American customers in Latin America. They develop regional footprints, sourcing from more locations. They pay closer attention to the complexities associated with each territory’s laws and regulations, including its political and economic stability. They make their operations more flexible and take advantage of regional trade blocs and agreements.

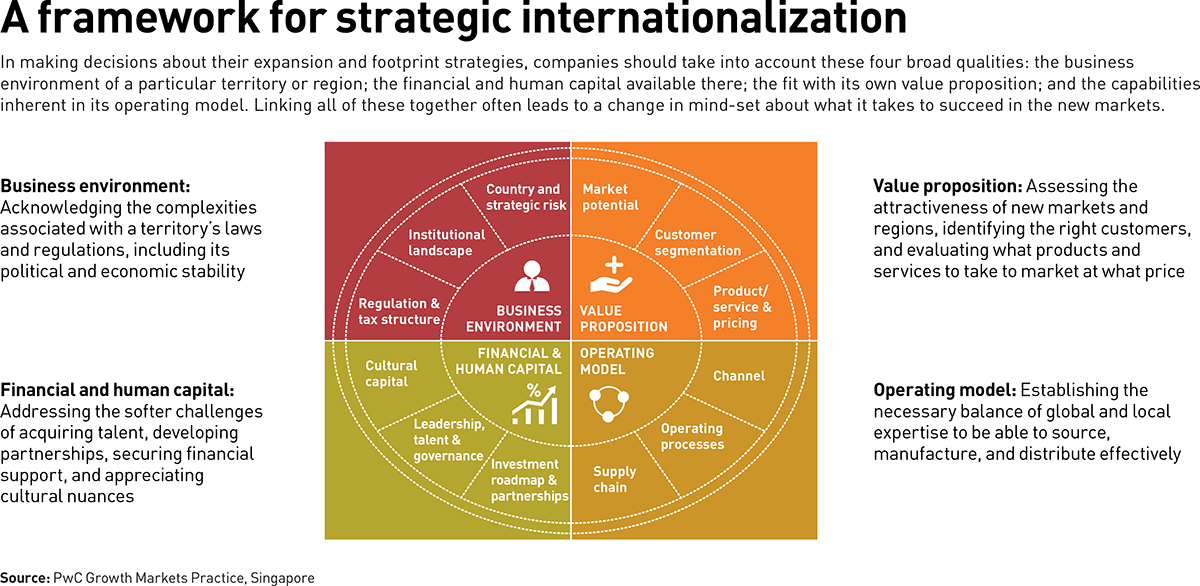

This approach opens new opportunities for governments to take a fresh look at the capabilities and strengths of their industries and people, and carve out a winning position for themselves as attractors of trade and investment. Some governments, such as those of Bulgaria, Morocco, Serbia, Tunisia, and Vietnam, are already demonstrating by example how to accomplish this. A framework of internationalization is taking shape, in part at PwC’s growth markets practice, to help articulate how a country’s or territory’s inherent advantages may now naturally come to the fore in business decision making (see “A framework for strategic internationalization”).

The headwinds of uncertainty

Globalization and international commerce have faced strong headwinds before, as author Pankaj Ghemawat notes in his book The New Global Road Map: Enduring Strategies for Turbulent Times (Harvard Business Review Press, 2018). High expectations for globalization and its benefits were deflated with the impact of the 1998 Asian financial crisis. A decade later, the global financial crisis was followed by calls for multinationals to “narrow their global presence,” Ghemawat writes.

It is even harder now for business leaders to decide where to invest for growth, as PwC’s CEO Survey shows. In addition to the fundamental shifts that are directing companies toward more regionalized operations, increasing nationalist and populist sentiment complicates matters, especially when it takes the form of cross-boundary regulation. The World Trade Organization (WTO) published a report in June 2019 showing that G20 nations had implemented 20 new restrictive trade measures between October 2018 and May 2019, including higher tariffs, import bans, and new customs procedures for exports. Those measures affected goods worth almost US$336 billion — the second-highest figure recorded since the WTO began tracking it in 2012.

Not only are the U.S. and China at loggerheads over trade, but trade disputes have flared between the Trump administration and Turkey, and, more recently, between Mexico and India. Japan and South Korea have lately gone head-to-head over Japanese exports of high-tech equipment in a row that could threaten global microchip supplies. A dispute even broke out in June 2019 between the unlikeliest of combatants: Scotland and Ireland, over fishing rights around an uninhabited piece of rock in the North Atlantic, hundreds of miles west of the British mainland.

Another factor affecting business planning is the current Chinese approach to sourcing. Historically, companies imported key components into China to be assembled by more affordable workers; however, over the past decade, Chinese suppliers have become more mature. This means that companies with plants in China can source quality components from within the country and do not need to import as much as before, a factor that has contributed to the trade deficit certain countries now have with China. In some industries, China is moving away from suppliers on which it has relied for two decades.

All this has had a chilling effect on international commerce. Imports by G20 economies were 1.2 percent lower in the first quarter of 2019 than they were a year earlier, whereas exports were only marginally (0.4 percent) higher, Organisation for Economic Co-operation and Development figures show. “The core problem is uncertainty,” said Piyush Gupta, chief executive of Singapore’s largest domestic bank, DBS, in an interview with strategy+business. “There’s a general environment of skittishness.”

Winners of the new game

At the same time that these headwinds are causing uncertainty for companies, however, another profound consequence appears to be a realignment of growth opportunities. Some businesses and territories whose attributes may have been overlooked before, or whose advantages now naturally come into play, have a chance to gain ground.

Consider Vietnam. Its textile factories, shrimp processing plants, and mobile phone manufacturers are operating at full tilt. Although business has been good for some years — thanks to a welcoming foreign investment policy, favorable demographics, and growth of an urban consumer class — commercial activity has spiked dramatically in 2019. In effect, Vietnam has suddenly become a beneficiary of tariff-related tensions between the U.S. and China. Its exports to the U.S., largely unburdened by tariffs, surged almost 40 percent in the first three months of 2019, compared with a year earlier, according to a Financial Times analysis of data from the U.S. International Trade Commission. For example, imports into the U.S. of Vietnamese-made mobile phones more than doubled, year-on-year, while those from China fell noticeably. This has helped drive a more than 45 percent jump in Vietnam’s trade surplus with the U.S. in the first quarter alone.

Vietnam is one of eight Asian economies to have benefited hugely from the new trade uncertainty. Total exports to the U.S. from this group — which also includes Bangladesh, India, Indonesia, Malaysia, South Korea, Taiwan, and Thailand — grew by 16 percent year-on-year in the first quarter, according to the July edition of PwC’s Global Economy Watch.

But 2019’s trade war is probably not the most pivotal factor; it is adding urgency to a change in supply chain footprints that was already underway. Since as far back as the 2008 financial crisis, many companies have gradually been moving their supply chains away from China. Harley Seyedin, president of the American Chamber of Commerce in South China, was reported in the Financial Times as saying that the 2019 trade war was only accelerating investment decisions that had already been on the drawing board. This approach has even gotten a name: the “China-plus” strategy. Indeed, most countries in the Association of Southeast Asian Nations (ASEAN), of which both Vietnam and Cambodia are members, have enjoyed varying degrees of economic growth for the same reason.

From global to regional

To more fully understand today’s change in global trade, it’s important to look at fundamental factors. One is simply the maturation of more developing markets, combining increasingly sophisticated manufacturing capabilities with relatively low labor costs. Developing economies — in Africa, Latin America, and ASEAN — can now supply one another with goods far more easily than they used to. Just two decades ago, 62 percent of global bilateral trade was conducted by the U.S., Canada, and Europe. According to a Bloomberg analysis of U.N. Comtrade data, that share has now gone down to 47 percent.

Vietnam has suddenly become a beneficiary of tariff-related tensions between the U.S. and China. It is one of eight Asian economies to have benefited hugely from the new trade uncertainty.

With that shift in supply has come an expansion of consumer demand in the same countries. In emerging regions such as North Africa, Central and Eastern Europe, India, and ASEAN — which has a population of 620 million people — an increasingly affluent middle class, with more disposable income, has shifted its consumption profile. Manufacturers in these regions can rely less on consumers from developed regions such as the U.S. and Western Europe. Manufacturers need to be located closer to these consumers, to respond rapidly to their more sophisticated expectations.

Other factors have contributed to regionalization. Governments are increasingly seeking regional trade agreements. Infrastructure is improving, including the development of supply chain platforms with new Industry 4.0–style technologies. Tighter regulations on emissions in China have pushed some manufacturers elsewhere. Labor costs are no longer the sole determinant of where supply chains are based. Other factors are coming into play, most of all where consumers live.

“Long-term trends…suggest it is becoming increasingly important to think about the world in terms of regional groupings,” writes Ghemawat. A flat-screen TV sold to a consumer in an ASEAN country might now be made in a nearby country, whereas one sold in Western Europe is made in Central Europe and one sold in the U.S. or Canada is made in Mexico.

Capital-intensive investment decisions are increasingly made with regional economics in mind. Ineos, a large, privately held chemical producer, recently announced it would make its first investment in the Middle East by spending $2 billion to build three petrochemical plants in Saudi Arabia, the largest economy in the region and one with a rapidly growing consumer class. The investment by Ineos will include a state-of-the-art facility to make acrylonitrile, a thermoplastic that is a key ingredient in the manufacture of clothing and carpeting, and commonly used in automotive components, phones, and computer casings.

Another manifestation of this trend is the creation of regional value chains (RVCs). In Africa, work has been underway in recent years to develop such chains as a way of boosting intraregional trade in agricultural commodities. Participation in RVCs allows enterprises to gain economies of scale more rapidly, and thus attract the investment they need to innovate.

These fresh opportunities are meaningful for government as well as businesses. Jurisdictions around the world have much to gain from this year’s great dislocation. Some may find opportunities to profit from their geographic position — for example, if they are juxtaposed between the U.S. and China, which are still the largest actors in the global economy. Others may be positioned to take advantage of the new regional trade flows and supply chains.

Examples of governments already positioning themselves include Singapore, which aims to capitalize on the supply chain shift from China toward ASEAN. Beh Swan Gin, chair of the city-state’s economic development board — a government agency responsible for attracting inward investment — told the Financial Times that his agency was “thinking beyond our borders” to see how to “create a supply chain in Southeast Asia that can benefit manufacturers in Singapore.”

Neighboring Malaysia is also preparing itself for a permanent reorientation of the supply chain, according to finance minister Lim Guan Eng. In remarks at an awards dinner in mid-2019, he predicted that the current trade uncertainty would lead to a global growth upswing, which his government could take advantage of. “We are readying ourselves two steps ahead,” he added. “We are preparing for the worst of the trade war, and what comes next five to 10 years down the road.” Thailand, similarly, is instituting a “relocation package” composed of tax incentives, economic zones, and legal changes, all designed to invite companies to move production or consider other forms of investment.

Opportunities in stability

Promoting a business-friendly tax regime, a rule of law, and a well-designed foreign investment framework are established attributes for attracting foreign direct investment (FDI). But five additional factors may be particularly helpful for territories around the world in these uncertain times.

Stability is the first. To be sure, multinationals and other corporations have always valued this, but it comes at a premium in today’s volatile environment.

One instructive example is Central and Eastern Europe (CEE). Since the fall of the Berlin Wall in 1989, the region has benefited from a steady increase in inflows for investors, and gross domestic product (GDP) growth has recently outperformed that of many Western European economies. Currencies in most CEE countries are stable, wage levels are highly competitive, and IT-savvy young graduates are plentiful. Each country has a relatively strong consumer market and, importantly, is politically stable.

Bulgaria, for example, has made a virtue of its stable currency — and low taxes — by turning itself into a large hub for automotive parts manufacturing. Lufthansa operates a European aircraft maintenance center for narrow-body, short-haul aircraft near the Bulgarian capital, Sofia. The location allows the German airline to service customers in a regional catchment area in a radius of around 5,000 kilometers, taking in the whole of Europe, Russia, the Arabian peninsula, and North Africa.

Indeed, some might argue that the CEE region, as a whole, is looking more stable than Western Europe this year. It was notable in PwC’s CEO Survey that “populism” did not feature among the top three concerns for CEOs in CEE — but it was cited among the top three threats for respondents in Western Europe. Indeed, Brexit continues to cause considerable political instability in the U.K., Spain is grappling with a fractured party system, and the emergence of right-wing populism — notably in Italy and Germany — has shaken the foundations of moderate, mainstream political parties across Europe.

In North Africa, stability has also been a driver for investments in some territories at a time when the wider continent’s growth has been slowing. According to the latest World Investment Report (pdf) from UNCTAD (the United Nations Conference on Trade and Development), in 2018, FDI flows into North Africa rose by 7 percent compared with the previous year, to $14 billion.

Two locations — Morocco and Tunisia — stood out. The former saw inflows rise by 36 percent as the Moroccan economy benefited from relatively stable economic performance and diversification; it is drawing FDI in finance, renewables, and automotive. Tunisia’s inflows rose by 18 percent, and it is benefiting from a five-year plan to encourage investment in aircraft and car components, textiles, health and education, and tourism.

Tourism and good governance

Tourism is the second factor — and there is an interesting story to tell about it, particularly in the context of stability. In an analysis of PwC’s CEO Survey results, the firm’s U.K. economics team examined a range of more than 30 variables that may influence CEO decisions on which three territories have the highest potential for growth. The team collected a wide range of variables for each territory. These included GDP growth, unemployment rate, technological readiness, quality of infrastructure, the rate of non-performing bank loans (NPLs), and tourism.

In PwC UK’s research, tourism levels — as measured by receipts for travel items — showed a statistically significant positive coefficient in the results. “This suggests as tourism levels increase, CEOs are more likely to view that country as a ‘top-three’ territory for growth,” according to John Hawksworth, chief economist at PwC UK.

Indeed, although executives in other industries tend to underplay the importance of tourism and NPLs, these factors can be viewed as a proxy for other macroeconomic or financial factors. Tourism may be a proxy for the rule of law, which, as the study’s authors pointed out, “influences how safe people feel in a country.” NPLs, for their part, may indicate the robustness of the financial system and associated regulatory regimes.

The example of Africa points toward a third factor: good governance, including investment reform. Investors always place a high value on jurisdictions, especially in emerging markets, that are prepared to carry out structural reforms that will enable the flow of capital and trade in goods and services. This could be particularly important for territories that have hitherto not been top-of-mind for global businesses.

A continent-wide analysis of economies in Africa appearing in PwC’s Global Economy Watch early in 2019 looked at how levels of governance related to economic growth on the continent, and found a direct positive correlation. Three of the fastest-growing economies — Cote d’Ivoire, Rwanda, and Guinea — saw the strongest improvements in their governance indicators. Improving governance across Africa could be key to economic development, and PwC estimated that these gains could be worth $23 billion in added GDP if the governance improvements in each African economy were realized to the extent that they had been in Cote d’Ivoire, over the five years up to 2017.

Brazil, the largest economy in Latin America, may turn out to be another example. Although it may have experienced market volatility due to recent elections, the lower house of its National Congress passed landmark pension reform in August 2019. It must still be passed in the upper house, but the move appears to have boosted confidence that this might help Brazil restore growth, especially given that it took 20 years to get the legislation to this point.

Services and digitization

The fourth factor that may help territories succeed is services, especially those involving information technology. For many governments, the creatively disruptive effects of what PwC calls the essential eight technologies — including artificial intelligence (AI), the Internet of Things, virtual reality, and drones — are increasingly vital to national economic development as global value chains shift from being based on manufacturing and goods to services and areas such as research and development.

As pointed out in Gravity without Weight, (pdf) a 2019 PwC report on the effect of distance in global trade, the recent proliferation of tradable services such as offshore call centers, online accounting software, and legal and consulting services means that these services are more important to the world economy than ever before. Territories that either have inherent advantages here or have ambitions to develop them could be in a sweet spot. Serbia, a relatively small country in southeastern Europe deeply affected by regional conflicts in the 1990s, has used low wages and employee subsidy schemes to attract investors in information technology since then, and now generates 10 percent of its GDP from the sector.

Another strategy could involve territories that may have been reliant on single drivers of their economy — such as energy — adopting a holistic strategy focusing on a new national agenda. In the Middle East, PwC has developed a model called in-country value (ICV) — already implemented in oil-rich Qatar — that aims to catalyze the economic value within a country through developing local companies and human resources in an effort to reduce reliance on imported goods and services and attracting inward investment.

Finally, the digitization of government and public services is a fifth factor that can help unlock opportunity. In its latest flagship Doing Business report, (pdf) the World Bank notes that four economies among the top 10 improvers in sub-Saharan Africa — Côte d’Ivoire, Kenya, Rwanda, and Togo — had digitization as a common theme among their business regulatory reforms.

Côte d’Ivoire and Togo introduced online systems for filing corporate income tax and value-added tax returns, and Kenya simplified the process of providing value-added tax information by enhancing its existing online system, iTax. Rwanda streamlined the process of starting a business by replacing its electronic billing machine system with new software that allows taxpayers to issue value-added tax invoices, the report said.

The overarching aim should be the creation of a new breed of digital public services designed to meet the needs of citizens. They should be built around five core values, laid out in a recent PwC research project on the future of government in Britain. It said these digital services should be:

• Intelligent — using AI to proactively drive early interventions to support the most vulnerable in society.

• Informed — joining up data to support government to make better decisions and provide more efficient and effective services to those most in need.

• Interactive — moving beyond online forms to provide richer, more valuable interactions with citizens, helping them navigate services and providing them with options for delivery.

• Integrated — breaking down traditional boundaries between government departments to create interactions with citizens in ways that make sense to them.

• Identity-secured — providing a secured digital identity for all citizens, to ensure the trust is there to provide the foundation for digital public services.

Looking inward to exploit advantages

As CEOs scan the globe, they may have a tendency to view territories as holistic entities, and to overlook regional differences within them. Instead, territory governments should look inward, thinking about which of their regions could gain the most from these new territories.

India’s vast size is an obvious obstacle to any attempt to treat the country as a single entity: Its 1.3 billion people are spread across a federation of 29 states, some as big and productive on their own as entire countries. What’s more, each state has its own distinct culture, history, mix of dialects, and array of industries and business environments. Uttar Pradesh, a state in northern India that is home to the Taj Mahal, has a land area comparable to that of the U.K., and Karnataka in southern India — famed for its high-tech megacity, Bangalore — has a state economy comparable to that of Portugal.

Paying this kind of attention to Indian states is vital, because they have a significant influence on the business environment, with their own government, courts, taxes, and regulation. Indian government reforms, under recently reelected prime minister Narendra Modi, have put the onus on state governments to create conditions for business growth, with the emergence of “competitive federalism” between the states as they each strive to sharpen their attractiveness to inward investors.

Thailand, meanwhile, is focusing on developing an “Eastern Economic Corridor,” a new special economic zone geared toward advanced technology such as aviation and automation, which spans three coastal province seats of the capital, Bangkok. Public and private funds totaling more than $45 billion are to flow into infrastructure projects — airports, deep-sea ports, and high-speed railways — in a bid to spur national growth that has lagged behind regional peers in recent years.

Meanwhile, for many businesses surveying the globe for growth, the new challenge is a disarmingly simple one: to be able to invest in places where their money “isn’t going to blow up,” in the words of one veteran observer. Opportunities are opening up for governments throughout the industrialized world, which now have an opportunity to reposition themselves to capture attention.

For example, Canada rose in PwC’s CEO Survey ranking of growth market opportunities. It has quietly been taking advantage of a visa-related brain drain effect northward from its neighbor, thanks to “America first” hiring and visa policies. Toronto, the country’s largest city, has created more tech jobs than San Francisco in the past two years, and there are 200,000-plus more tech jobs clustered along the 100 kilometer–long Toronto-Waterloo Region Corridor in Ontario.

For businesses, a strategy based on internationalization will mean shifting supply chains to serve new consumer markets with products that are manufactured with regional suppliers, as well as being flexible enough to manage rapid changes in tariffs and other geopolitical shifts. The winning governments will be those that are open for business, in a way that leads companies to find them and settle into a pattern — now and ideally into the future.

Author profiles:

- David Wijeratne is a partner with PwC Singapore. He leads PwC’s growth markets practice, a global team supporting companies’ efforts to expand internationally.

- Jeremy Grant is international editor of strategy+business.